Glenigan data shows construction volume output reaches pre-pandemic levels

Construction volume output rises 3.5%, reversing October’s 1.7% decline.

- Value of detailed planning consents in Q4 rise by (26%) against preceding quarter

- Major contract awards increase 13% against Q3, up 11% on a year ago

- Value of main contracts awarded increases 4% against previous three months, up 7% on last year

- Value of projects starting on site for Q4 dips 39% on Q3, 23% lower than a year ago

- Industrial project-starts continue to perform strongly, up 37% on same time in 2020

- Construction volume output rises 3.5%, reversing October’s 1.7% decline

The latest report from Glenigan from the three months to the end of December 2021 shows whilst the value of Q.4 project starts fell 39% on Q.3, detailed planning consents rose over a quarter (26%) and main contract awards were up 13%, indicating a robust pipeline of work in Q.1 and Q.2 2022.

Further, Construction volume output rises 3.5%, reversing October’s 1.7% decline. This upturn brings monthly output back to pre-pandemic levels, suggesting supply chain issues, which has hindered construction activity throughout most of 2021, have eased.

Planning consent and approvals on the rise

Despite a weak end to 2021, built environment professionals should be encouraged by a healthy increase in the value of detailed planning consents, which rose by over a quarter in Q4 (26%) against 2021’s Q3.

Major planning approvals (projects over £100million) also rose by 46% during the three months to December, but were down 41% on a year ago. Underlying planning approvals (projects under £100 million) also grew 7% on the previous quarters, 8% higher than 2020 figures during the same time period.

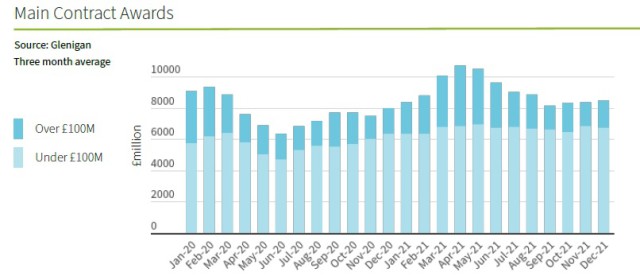

The value of main contract awards increased in 2021’s Q4, up 4% against Q3, and was 7% higher on 12 months ago. It’s worth noting that awards for projects under £100 million also edged up 5% on last year’s figures, but were 11% down on Q3 in 2021.

Industrial project starts stand out

Although overall project starts dropped a sizeable 39% against Q3 during Q4 2021, underlying industrial starts (less than £100 million) continue to perform strongly. Only down 1% on a strong third quarter, they are also up 37% against the same period in 2020.

Infrastructure starts were also encouraging, increasing 15% against Q3, but were still 25% lower than a year ago.

It’s clear project starts in Q.4 have been negatively affected by ongoing supply chain issues, which have continued to cause sector-wide disruption, prompting builders to delay starting new projects. However, a healthy development pipeline should see a rise in project starts over the medium term.

Sector output shows growth

Looking at the wider context. According to official data from ONS, the volume of construction output bounced back significantly in November, rising 3.5% and reversing October’s 1.7% decline. This is good news for the sector, with overall output rising by 1.6% against 2021’s Q3, up 6.3% on the same time period one year ago.

Particularly, new work output rose by 1.5% during the three months to November in 2021, pushing it up 7.1% on 2020 figures. New work activity has been spurred by increases in infrastructure (3.6%), public non-residential (5.2%) and industrial work (11% SA) against the preceding three months.

Repair and Maintenance work also grew 1.6% during the three months to November 2021, up 6.3% on 2020 figures. The rise was led by a 2.0% and 1.5% RM&I (repair maintenance and improvement) increase in private housing and non-housing respectively.

By the same token, residential new work edged higher throughout Q4 2021, with a 1.8% rise in private new housing output. This was partly offset by a 7.5% drop in social housing work.

Furthermore, the picture isn’t as positive for commercial output which dropped 3.2% (SA) in 2021’s Q4 against Q3, dipping 12.2% on a year ago.

Regional Analysis

London (+15%), Wales (+12%) and the South East (+8%) were the only areas to experience growth against the preceding quarter. All other regions saw a consistent decline in line with a downward trend, first registered in Autumn 2021.

Particularly, project starts in Northern Ireland fell sharply against the preceding quarter (-20%), despite increasing 30% compared to the same period in 2020. Scotland, (-42%), the East of England (-38%), the South West (-32%) and the East Midlands (-30%) saw similarly steep drops against the previous year.

Commenting on the findings, Glenigan’s economic director, Allan Wilen, said: “Considering the challenges that have been thrown at the construction industry throughout the year, it’s been able to weather the storm and show its resilience. The rise in construction output, planning consents and approvals are welcome news and paint an optimistic picture for the future after a very difficult end to the year. Signs that supply chain issues are easing off supported by a strong development pipeline, indicates the industry is in a strong position as 2022 dawns.”