Building-controls market tops out

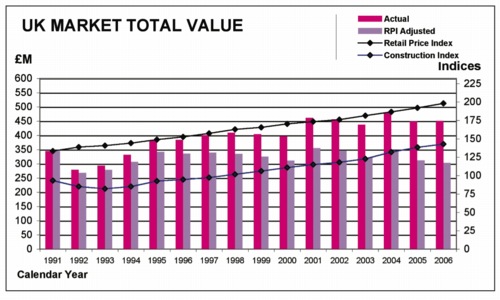

The role of system installers in the market for controls and building-management systems is growing, according to figures compiled by the Building Controls Industry Association — but service and maintenance work shows a sharp decline.This time last year the Building Controls Industry Association (BCIA) reported that for the first time since records began in 1991 the industry had experienced below-par growth. This year’s market report, based on 2006 figures, shows an equally stagnant trading period. The total value of products, installed systems and service and maintenance supplied into the UK market during the 2006 calendar year was £451 million, an increase of £1.5 million (0.33%) from 2005.

|

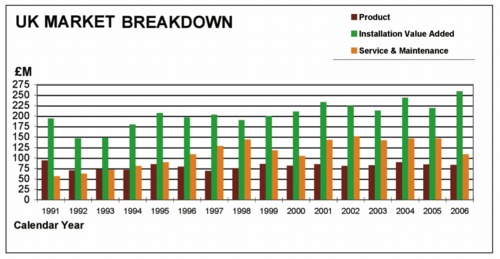

While the value of product sold for controls and building-management systems remains virtually unmoved, the installation value added has grown — but services and maintenance work shows a sharp decline. |

A major shift in the profile of the building controls market has been the decline in service and maintenance, with greater emphasis on the installation of new systems. This may well be a bright indicator for the future of installed-systems business, with the knock-on effect of increasing service and maintenance in the following years. However for 2006, service and maintenance showed a sharp decline, with total control and BMS revenue falling by 25.5% from the 2005 level of £146 million down to £109 million. The division between controls manufacturers and system installers is 48.3% (manufacturers) and 51.7% (installers).

Control and BMS product With the exception of sales to systems installers, the value of product supplied into the market via manufacturers’ own installed systems, OEMs, and distributors fell. Manufacturers’ systems experienced the largest drop at 3.9% to £20.6 million, sales to OEMs were down 2.7% to £9.1 million, with sales to distributors declining by 1.5% to £13.9 million. The marginal rise in sales to systems installers of 0.34% to £39.5 million resulted in an overall decline in control and BMS product of 1.39% at £83.1 million, which represents a virtually equal RPI-adjusted fall of 1.43% in real terms.

Installed systems There was better news from on revenue for total primary systems, based on product either installed by manufacturers themselves or supplied by them directly to systems installers, which rose by 12.4% to £274 million — significantly surpassing the provisionally indicated 3.2% annual rise in the DTI ‘All construction index’ (CI). Within the total sales value of primary systems, manufacturers’ revenues increased by 3.4% to £108 million, with systems installers experiencing a significantly higher rise of 29.2% to £167 million. Share of the market saw a decrease for manufacturers to 39.2% and an increase for systems installers to 60.8%.

|

Perhaps driven by the ever-increasing value for money of micro-electronic equipment, the UK market for controls and building-management systems has not only fallen below the RPI index but also below the construction index. |

Value added for system engineering, panels, installation and commissioning within primary-systems revenues increased from 74.5% (2005) to 77.8% (2006) of average system price. This change shows a slight increase from 79.4% to 80.8% for manufacturers’ installations and a much greater increase from 71.8% to 76.3% for systems installers’ installations. Total value added within all installations increased significantly, by 18.2% (£39.8 million) up to £259 million and was a major contributor to achieving an overall market value above that of 2005. Consequently, overall product value declined to an average of 22.2% of the installed price, while system engineering and commissioning rose to 27.1%, and panels, wiring, peripherals, and installation increased to 50.7%.

Summary To summarise the 2006 UK home market compared to 2005: • Product sales to OEMs decreased by 2.7% to £9.1 million.

• Product sales to distributors decreased by 1.5% to £13.9 million.

• Product sales to systems installers rose by 0.3% to £39.5 million.

•Product included in manufacturers’ own installations decreased by 3.9% to £20.6 million

• The overall value of all product supplied into the market decreased by 1.4% to £83.1 million.

• Primary-installed-systems revenues rose by 12.4% to £274 million.

• Manufacturers’ share of primary systems declined to 39.2%, while that of system installers’ rose to 60.8%.

• Value added to engineer, install and commission systems, rose by 18.2% to £259 million.

• The total value of all installations rose by 13.2% to £333 million. • Control and BMS industry revenue for service and maintenance revenues fell by 25.5% to £109 million.

• Manufacturers’ share of service and maintenance fell to 48.3% while that of systems installers rose to 51.7%

• All product and service and also maintenance revenues fell by 16.6% to £192 million.

• Total revenues for the control and BMS industry increased by 0.33% to £451 million. Setting the above figures in the context of the overall performance of the construction industry, for which the provisional indices from the Department of Trade & Industry indicate increases in public, private industrial and private commercial works of 2.7%, 2.5% and 2.2%, respectively, the overall increase in installed-systems business was very satisfying. However, the increase in installed systems was almost overshadowed by the decline in service and maintenance.

Related links: