Whole-life costing guides investment in energy efficiency

KATHRYN BOURKE and MIKE CLIFT discuss whole-life costing against the background of pressure from the Government for public-sector procurement to be based on this philosphy.Whole life costing (WLC) involves assessing the total cost of a building or its parts throughout its life (including the costs of planning design, acquisition, operations, maintenance and disposal), less any residual value (BS/ISO 15686-1:2000 Buildings and constructed assets — Service life planning Part 1: general principles) Its key elements can be summarised as follows. • What needs doing? • When should it be done? • How much will it cost? It is a tool to help make decisions between different options with different costs that may occur at different times over a period of time. Whole-life costing is relevant when considering whole estates, whole facilities, individual buildings or components.

Public-sector client demand for whole-life costs There is a lot happening in the area of whole-life costs. In particular, there is pressure from the highest levels of Government for public-sector procurement to move to an approach based on whole-life cost. The Office of Government Commerce (OGC) Procurement Guide 07 (1) provides public-sector procurers with guidance on whole-life costing. HM Treasury’s Green Book (2) states that when valuing the costs and benefits of options, such costs and benefits should normally be extended to cover the period of the useful lifetime of the assets being evaluated (i.e. whole-life costing). The Energy White Paper 2003 (3) states that the UK is using far more energy than it needs and that around half the total carbon savings required by 2020 should come from energy efficiency, with households accounting for half of these savings. The Government is pushing for local authorities to give energy issues priority at a strategic level, for example through their community plans and transport and housing strategies.

Component level At individual component level (Fig. 1), the whole-life cost is initial installation cost (either as new or as a replacement) plus the costs of inspecting, operating and maintaining it and its replacement cost when it wears out. In the case of a boiler, the initial installation cost is added to inspection, maintenance and parts replacements over its expected life. A boiler needs to be checked and maintained in accordance with guidance in HVAC specification, and its parts replaced on a regular basis. When the costs of these activities are getting out of hand, the unit is replaced, preferably before a complete breakdown if it is vital for the functioning of the building. It is important to capture all the activities associated with the ownership of a component if it is to last its normal life expectancy. Maintenance is costly and often put off because of budget cuts. This can result in backlog maintenance costs which would include the cost of the additional repairs due to the deferred maintenance.

Whole-building level At whole-building level, the whole-life cost is arrived at by adding up the initial capital cost of a building, inspection, operating and maintenance costs of all the individual components (windows, heating plant etc.) over their useful lives, plus the replacement cost at the end of life. These costs are usually presented at today’s costs by discounting the total sum. Some components in the building will impact on others. For example, a highly thermally insulated wall may (but will not necessarily) have a higher whole-life cost than a standard wall. However, this may be compensated for by the reduced heating costs. The higher standard wall may also reduce the required boiler capacity, with further cost savings attributable to the lower capital and replacement costs.

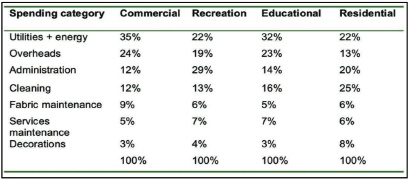

Quick wins The breakdown of operational costs in Table 1 indicates the major areas where savings can be made. Average figures, provided by Building Maintenance Information (BMI) (4), indicate that occupants’ spending falls into a number of categories for different building types.

Table 1: Cost of ownership by building type.

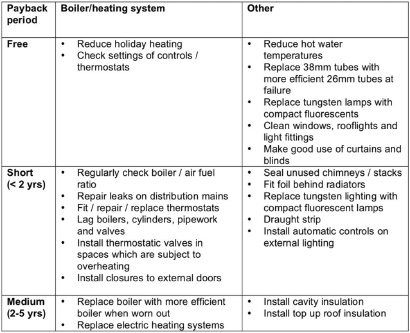

The Energy Efficiency Best Practice programme has in the past published guidance indicating that organisations in most sectors should be able to make average savings of about 30% over their previous energy use, with an average payback period of less than three years. At least half the savings are from simple low-cost measures with much shorter payback periods. The savings are even greater, and capital costs less, if options are chosen at design stage and integrated with the main building work (Table 2).

Table 2: Examples of typical payback periods for a range of energy-efficiency measures.

More examples of savings can be found on the Action Energy part of the Carbon Trust website.

Kathryn Bourke and Mike Clift are with Building Research Establishment, Garston, Watford WD2 7JR. cliftm@bre.co.uk This article is based on guidance prepared for EST — the Energy Savings Trust.

Related links: