Underlying project-starts uptick indicates gradual recovery, Glenigan data suggests

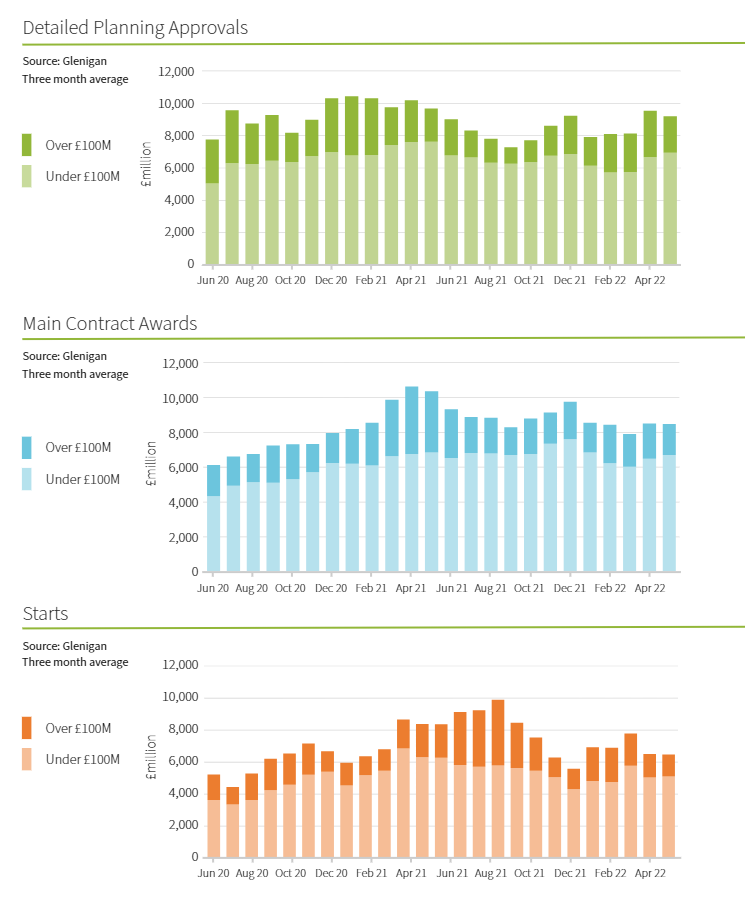

- 13% rise in detailed planning approvals against the preceding three months

- 18% decline in main contract awards against the previous year

- 9% increase in underlying starts during the three months to May

Glenigan has released the June 2022 edition of its Construction Review.

This review focuses on the three months to May 2022, with underlying figures seasonally adjusted.

It’s a report providing a detailed and comprehensive analysis of year-on-year construction data, giving built environment professionals a unique insight into performance over the last 12 months.

The central finding of June’s Review is a slight uptick in project-starts, increasing by almost a tenth during the three months to May, indicating signs of sector recovery following a gloomy few months in Winter/Spring 2022 and almost a year of steady decline.

Whereas project-starts have only recently shown signs of revival, a strong development pipeline of planning approvals and contract awards has been building up over the past 12 months.

Once again, both were up on the preceding three months, 13% and 1% respectively, giving cause for optimism entering the second half of the year.

Baby-steps to recovery

The June Review is quietly optimistic, presenting a more positive outlook than recent editions of this report.

However, whilst underlying project-starts performed well (+9%), the overall value of work commencing on-site averaged a modest £6.54 billion during the three months to May, falling 5% compared with the preceding three months, to stand 22% lower than the same period in 2021.

Highlighting the industry is not out of the woods yet, major project-starts (>£100 Million) accounted for this decline, dropping 32% against the previous three months, down 31% against last year.

Whilst overall main contract awards (+1%) and detailed planning approvals (+13%) were also up against the preceding three months, both stood lower than the same time a year ago, -18% and -5% respectively.

Drilling down into these numbers, major project approvals were down 5% on the previous three month period, but up by a tenth compared to last year. Vice-versa, underlying approvals experienced a solid increase of 15% during the three months to May, despite the value remaining 9% lower than the same time in 2021.

Major contract awards performed poorly falling 19% during the three months to May, standing a steep 49% lower than the previous year. Additionally, underlying main contract awards increased 11% against the previous three months, although stood 2% lower on a year ago.

A Curate’s Egg, June’s results highlight full recovery is still some way off. External influences, including the ongoing Russia-Ukraine War, Brexit related skills shortages, global supply chain issues and depressed consumer confidence are continuing to negatively affect output, as well as driving up inflation of construction materials prices by around 25% a year-on-year.

Sector Analysis - Residential

Underlying performance across sector verticals was mixed. However, some bright spots have appeared, particularly the residential sector, where project-starts performed well against the preceding three months, rising 24%.

This growth is largely attributed to a spike in private housing activity, which experienced the largest growth of any sector (+45%) during this period. Despite this, the value of both overall residential and private housing project-starts remained lower than 2021 figures, experiencing a decrease of 24% and 23% respectively.

Social housing-starts also performed poorly, also experiencing a 23% decline in the three months to May, standing 32% lower than a year ago.

Sector Analysis – Non-Residential

In the non-residential sector, performance was relatively poor. Office project-starts continued to be the highest performing vertical, experiencing 27% growth during the three months to May, but sitting 3% lower than a year ago.

Retail and health construction also saw positive growth, both registering a modest value increase of 1% and 8% respectively against the preceding three month period. However, retail remained 17% lower and health unchanged compared with the same time last year.

Despite the hotel and leisure’s extremely strong performance at the start of 2022, project-starts in this vertical experienced the greatest fall, plummeting 30% compared with the preceding three month.

Civil engineering work starting on-site experienced a relatively small decline, 5% down against the preceding three months, but remained 25% lower than a year ago. This can be partly attributed to a fall in utilities project-starts (-2%) in the three months to May. Utilities also suffered the second greatest decline against the previous year, falling by nearly a third (-29%).

Infrastructure work was also down 24% on 2021, with work starting on-site slipping back 6% against the preceding three months.

Regional Analysis

Regionally, the outlook was optimistic, with project-start levels improving across the UK, including the South East which experienced a value increase of 30% against the preceding three months. Despite being 2% behind 2021 output levels, this was the strongest growth of any region.

Up 21%, Wales also experienced a strong three months to May, and was the only region in the UK to experience growth against both periods, increasing 13% compared to a year ago.

The South West was another strong performer, with work commencing on-site increasing 25% against the preceding three months, despite falling by the same amount against 2021.

In contrast, four regions performed poorly, including the North East which faltered on its strong output so far in 2022. Here the value of project-starts fell 18% against the preceding three months to stand nearly a third (29%) lower than the previous year.

London also experienced a significant decline of 29% against 2021, and a 13% decrease compared with the three months to May.