In search of efficient air conditioning

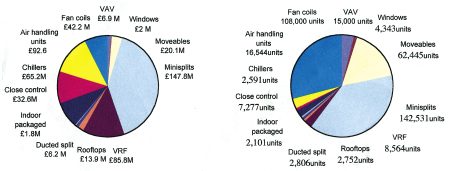

Both by value and by volume, minisplit air conditioners dominate the UK market — but the low-cost fan-coil unit remains prominent. These are BSRIA’s estimated figures for 2003.

Technical competition is joining price as one of the driving forces in the UK air-conditioning market. Ignacio de Alvaro has the details.The air conditioning market is showing signs of recovery in 2004, following the downturn experienced during 2002 and 2003. Two years ago, air-conditioning sales decreased by 6% to a value of about £510 million due to the poor economic performance across all sectors. The favourable weather conditions during the summer of 2003 boosted-air conditioning sales in the lower end of the market, which prevented further sales declines and allowed the overall market value to remain at similar levels.

Positive impact The better economic outlook for 2004 has had a positive impact on the air-conditioning market by generating new demand and reactivating jobs that were put on hold. First-quarter results are encouraging. The higher end of the market, especially the chillers market, is expected to benefit most from the recovery after two depressed years. Levels of competition have increased significantly across all product areas. Low-cost competitors have gained a notable share in the lower end of the market, particularly in the minisplit sector. This situation has generated continuous price drops over the last two years. Technical competition is also on the increase with suppliers, end users, government bodies and specifiers seeking for more ‘green’ and more efficient systems. Currently, the most comprehensive method to promote energy efficient air-conditioning products or technologies is the Enhanced Capital Allowance (ECA) scheme, which provides fiscal incentives to end users. The ECA is commissioned by the Carbon Trust and enables businesses to claim 100% first-year capital allowances on their spending on qualifying plant and machinery. From the supplier’s perspective, the ECA is a very effective marketing tool. However, the ECA scheme is in its very early days and needs to be extensively promoted so its benefits can be widely enjoyed across all businesses. Further, the Energy Technology List (ETL), which includes all products and technologies that meet energy-efficient criteria, often generates conceptual confusion within suppliers and end users due to its continuous development.

Energy labelling One of the European Community ways to promote energy efficiency is through so-called energy labelling. This initiative, valid since 1 July 2003, requires by law that a label must be displayed on all electrically powered heat-pump and cooling-only air-conditioning units up to 12 kW capacity. The label rates efficiency from A to G (A being the most efficient) and also shows the annual energy consumption of the system. This is a helpful tool for general end users with no particular technical knowledge to rapidly assess the efficiency of an air-conditioning system. We expect a gradual shift in the market to more expensive A and B efficiency and low cost units with lower efficiency F, G. With regard to technology improvements, the minisplit market is particularly exposed to innovation due to its relevance in the overall market. The most remarkable introduction in this sector has been the mini VRF. This type of system enjoys all the benefits that standard VRF systems bring, with outputs of only 3 to 7 hp and four to seven indoor units served by one outdoor unit. Mini VRF is 20% cheaper on average than standard VRF, which makes this product very competitive. Mini VRF fills in the gap between multisplits and standard VRFs. On the other hand, VRFs are gradually taking share from the lower end of the chiller market, and the rate appears to have accelerated in the last year. It is expected that Mini VRF will rapidly become popular, as more suppliers are introducing this range. So far, in the first six months of introduction, mini VRF sales have reached 10% share of the whole VRF market. Further, VRFs can enjoy the benefits of the ECA scheme since they have been recently included in the ETL. In the chiller market there is a growing trend towards small to mid-sized systems. Multi-compressor systems, often sold in modular formats, improve part-load operation. This allows end users to achieve cost savings by reaching higher efficiencies at low outputs. Also, end users currently lack drive towards extensive investments in air conditioning systems. In the lower end of the market, efficient part-load operation is mainly achieved by inverter technology, which represents about 30% of the splits market. Inverter technology allows the compressor to work at variable speeds for a better adaptation of thermal demands.

Free cooling Also, ‘free-cooling’ technology is expected to interest the market to make significant energy-cost savings. To achieve energy savings, the system monitors external ambient temperature and once this falls below the return-water temperature, the mechanical cooling requirement (i.e. the speed of the compressor) is reduced or, even, switched off if the cooling requirement is completely satisfied. The benefits of free cooling technology can be optimised for continuous cooling requirements such as IT rooms. On the other hand, the penetration levels of free-cooling technology are very low due to current low levels of market awareness. Also, free-cooling chillers cost 30% more (on average) than standard chillers. This price premium is difficult to justify in terms of financial return from energy cost savings.

Refrigerants In terms of refrigerants, there is a continuous move towards more environmentally friendly gases. The transition from R22 to HFCs, mainly R407C and R410A, is considered completed for split systems. R407C represents almost 60% of split systems and practically all VRF units. However, there is a trend pointing towards R410A as a predominant refrigerant in the future. The refrigerant picture in the chillers market is slightly more varied, although R407C appears to be the dominant refrigerant. Some players in the market show resistance to installing R410A systems. The performance benefits of R410A are largely a result of its higher operating pressures, which demands a more careful handling and running operation. Other than this, R410A offers a better EER (Energy Efficiency Ratio) than R22 or R407C. However, there continues to be some fears in the market that natural refrigerants will become mandatory in a few years.

Ignacio de Alvaro, is a market-research consultant, Worldwide Market Intelligence, BSRIA Ltd, Old Bracknell Lane West, Bracknell, Berks RG2 7AH ignacio.alvaro@bsria.co.uk

The views stated in this article are those of the author and do not necessarily reflect the stated policy of the company.

Related articles: