Market movement

Paul Burrows, Solutions Architect at the Building Cost Information Service (BCIS), takes a look back on labour costs and expected movement in 2025.

As rampant materials cost inflation – the most prominent feature of the post-pandemic construction landscape – has abated, labour has become the more significant cost driver on projects.

When construction demand is muted, as it has been recently, the industry self-balances, with workers moving to where the work is. Consequently, widely reported skills shortages have not been felt as acutely. However, with demand expected to rise again in 2025, pressures on the labour market may further impact costs.

What does the data show?

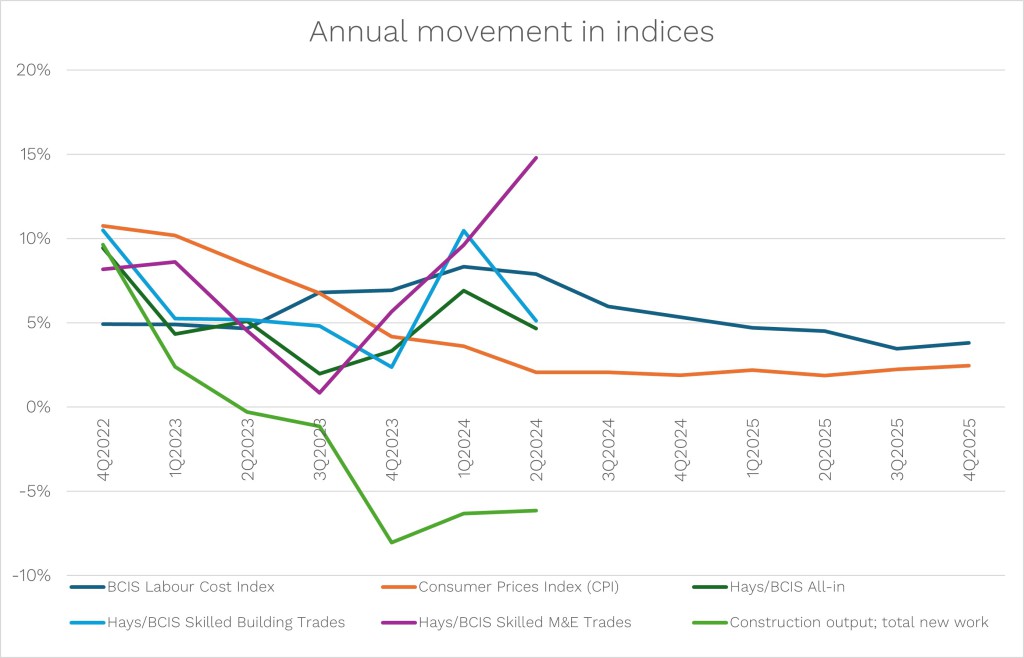

Annual movement in the BCIS Labour Cost Index peaked at 8.3% in the first quarter of 2024, the highest increase in over 20 years, reflecting changes in nationally agreed wage awards across the industry. Although the index has eased in recent quarters, it remained at 6% in Q3 2024.

We’re forecasting annual growth in the BCIS Labour Cost Index to ease to under 4% in the latter half of 2025. Demand levels in the industry and wider economic performance will of course have a bearing on longer-term changes.

A key method of tracking construction pay for BCIS has been through the Hays/BCIS Site Wage Cost Indices, launched in early 2020 and based on market data from Hays Recruitment. This data, reflecting movement in the agency labour market quarterly, tends to be more volatile and responsive to market conditions than other labour cost indices. Growth in the Hays/BCIS All-in index has been driven primarily by rising rates for skilled building and mechanical and electrical trades.

The Consumer Prices Index eased from a peak of 10.8% annual growth in 4Q2022 to 2.1% in Q3 2024, with wage awards across trades playing catch up in the intervening period. Plumbers, Heating and Mechanical Engineering Services (PHMES) operatives have seen the largest gains in the Hays data, followed by other skilled building trades, although this subset is comparatively small and tends to be more volatile.

Set against declining construction output, these increases underscore the impact of persistent skills shortages in these trades, with companies competing for qualified labour. Indeed, wage settlements for PHMES operatives have seen increases ranging from 7% to 8.2% in 2024. As construction output is projected to grow in most sub-sectors in 2025, further pressure on skills is anticipated.

What plans does Labour have for labour?

The government’s approach to addressing skills shortages focuses on upskilling the existing workforce, rather than relying on overseas labour. Plans include increasing apprenticeships and establishing Technical Excellence Colleges. Skills England, initially operating in shadow form within the Department for Education, aims to unite businesses, training providers and unions to ensure an adequate workforce. In place of the Apprenticeships Levy, a flexible Growth and Skills Levy is proposed, with Skills England consulting on eligible courses to ensure qualifications offer value. However, these initiatives will take time to yield tangible improvements, especially if overseas labour remains underutilised.

Sustainable construction needs skilled workers

The shortage of skilled workers is particularly acute in areas requiring specialised training, especially as the government aims to meet the UK’s Net Zero targets. New building regulations mandate heat recovery, electric vehicle charging points and heat pumps, increasing the services content in new builds and refurbishments.

The industry faces challenges in adapting to these changes and M&E work attracts a pricing premium, as reported consistently by the BCIS Tender Price Index panel, in part due to capacity constraints.

Outlook for the year ahead

As we move into 2025, construction output is expected to recover, but skill shortages will likely worsen before improving. While wage growth may moderate as inflation falls, demand for skilled labour will remain high. Adjustments to visa and immigration rules may provide short-term relief, but a long-term strategy is crucial.

Education and training, along with efforts to shift public perceptions about technical vocations, will be central to addressing these issues. It’s not solely the government’s responsibility; the industry must also invest in training and adopt a long-term recruitment view.

For now, employers must balance immediate needs with future demands, turning to recruitment specialists like Hays to help bridge skills gaps and secure the workforce necessary to meet the challenges of 2025 and beyond.